How Much House Can I Afford?

Learn how to estimate home affordability using income, debts, down payment, mortgage rates and monthly housing costs before you buy a house.

Quick summary

How much house you can afford depends on your income, debts, down payment, interest rate, loan term, property taxes, insurance and monthly budget. A common guideline is to keep housing costs near 28% of gross monthly income and total debt payments near 36%, but your personal comfort level matters too.

Key takeaways

- Home affordability is based on income, debt, down payment and total monthly housing costs.

- The 28/36 rule can help estimate a safe mortgage range.

- Do not rely only on the maximum loan a lender offers.

- A mortgage calculator helps compare scenarios before you shop for homes.

How much house can I afford?

A practical answer is that you can usually afford a house when the monthly payment fits your income, debts and lifestyle without putting pressure on your budget. Your affordable home price is not just the purchase price. It is the full monthly cost of owning the home.

That monthly cost may include principal, interest, property taxes, homeowners insurance, mortgage insurance, HOA fees, maintenance and utilities. Because these costs vary, two buyers with the same income may afford different home prices.

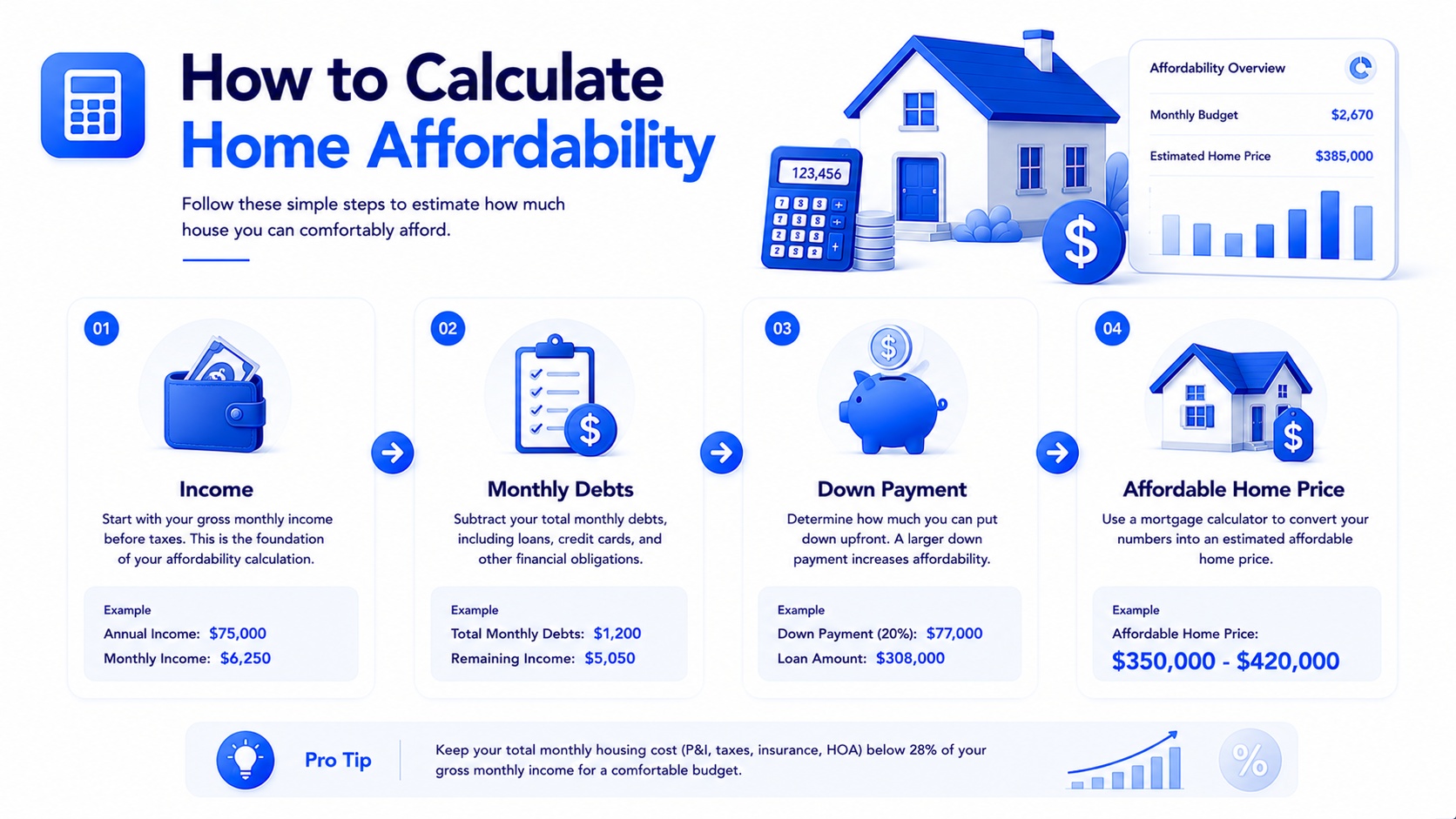

How to calculate home affordability

To calculate home affordability, start with gross monthly income, subtract existing debt obligations and estimate the monthly housing payment you can comfortably handle. Then test different home prices using a mortgage calculator.

| Input | Why it matters | Example |

|---|---|---|

| Monthly income | Sets the starting point for affordability | $6,000 gross monthly income |

| Monthly debts | Reduces how much payment you can safely handle | Car loan, credit cards, student loans |

| Down payment | Reduces loan size and may affect mortgage insurance | 5%, 10% or 20% |

| Interest rate | Changes monthly payment and total interest | Higher rates reduce affordability |

| Loan term | Affects monthly payment and total cost | 15-year vs 30-year loan |

Key factors that affect home affordability

Your affordable home price changes when any major mortgage input changes. A higher down payment, lower debts or lower interest rate may increase affordability. Higher taxes, insurance or debts may reduce it.

Income and debt

Lenders compare income to monthly debts to estimate how much payment may be manageable.

Down payment

A larger down payment can lower the loan amount and monthly payment.

Taxes and insurance

Property taxes and insurance can make two similar homes cost very different amounts each month.

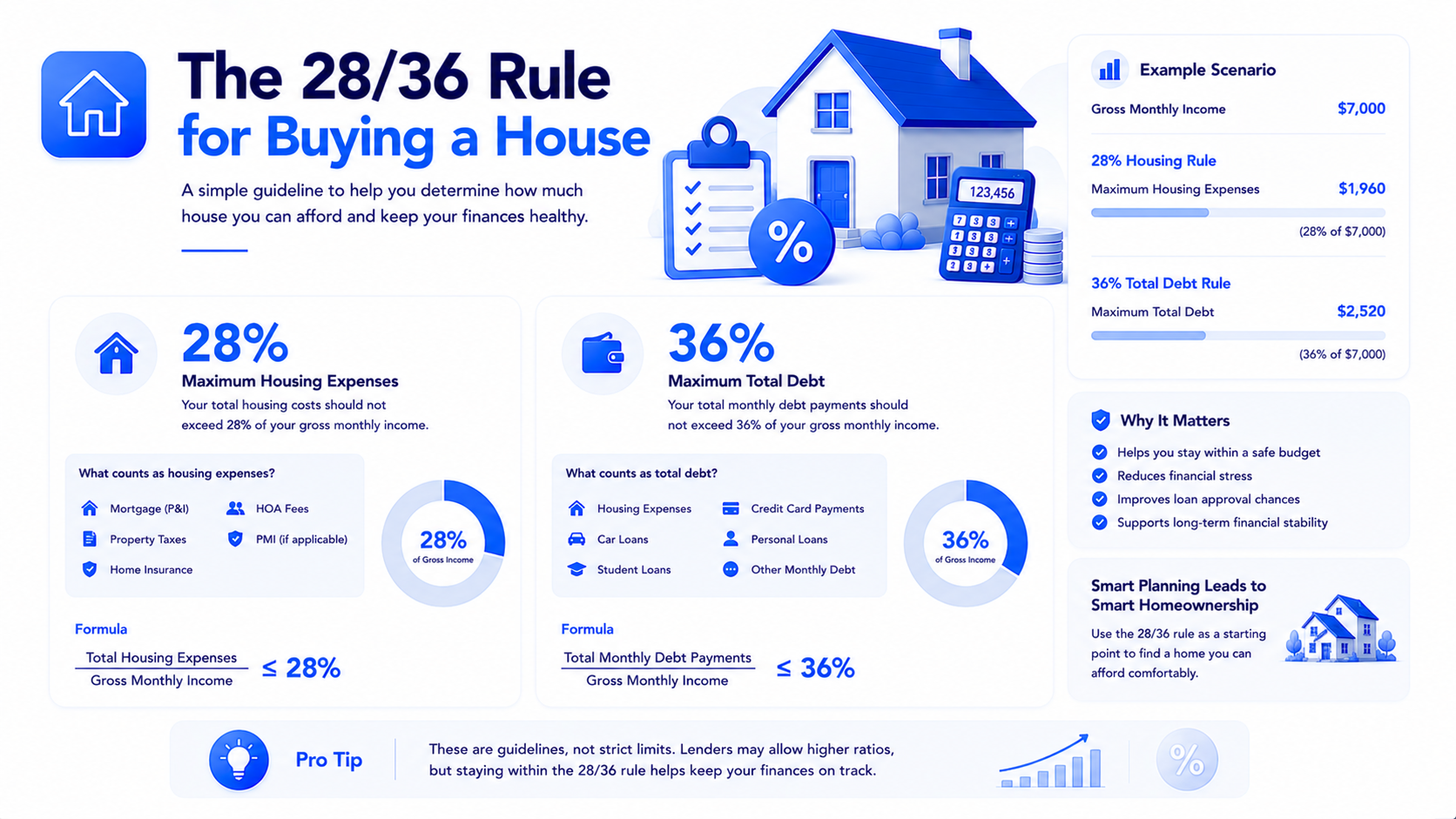

The 28/36 home affordability rule

The 28/36 rule is a common guideline used to estimate a manageable housing budget. It suggests spending no more than about 28% of gross monthly income on housing costs and no more than about 36% on total debt payments.

| Rule | Meaning | Example with $6,000/month income |

|---|---|---|

| 28% housing | Maximum suggested housing payment | $1,680/month |

| 36% total debt | Maximum suggested total debt payments | $2,160/month |

Common home affordability mistakes

Many buyers focus only on the home price or lender approval amount. The real question is whether the full monthly payment feels comfortable after everyday expenses and emergency savings.

Being approved for a large loan does not mean the payment is comfortable for your lifestyle.

Closing costs can add a large upfront expense that should be planned before buying.

Homeownership includes repairs, appliances, landscaping and unexpected costs.

Best practices before buying a house

Before choosing a home, compare mortgage scenarios, check your monthly budget and understand how interest rates change affordability. A smaller payment can provide more financial flexibility and reduce stress.

Compare scenarios

Test different down payments, terms and rates before deciding on a target price.

Build a buffer

Choose a payment that leaves room for emergencies, repairs and savings.

Shop mortgage offers

Comparing lenders may help you find better rates, fees and loan terms.

Estimate your monthly mortgage payment

Use The MuffinPost Mortgage Calculator Online Free to compare home prices, down payments, interest rates and loan terms before deciding how much house you can afford.

Open Mortgage CalculatorBrowse CalculatorsFrequently asked questions

How much house can I afford?

It depends on your income, debts, down payment, interest rate, taxes, insurance and monthly budget. A mortgage calculator can help estimate affordable scenarios.

What is the 28/36 rule?

The 28/36 rule suggests keeping housing costs around 28% of gross monthly income and total debt payments around 36%.

Should I buy the most expensive house I qualify for?

Usually no. Lender approval is not the same as personal affordability. Leave room for savings, repairs and lifestyle costs.

How does down payment affect affordability?

A larger down payment can reduce your loan amount, monthly payment and sometimes mortgage insurance costs.

Do taxes and insurance affect how much house I can afford?

Yes. Property taxes and homeowners insurance are part of monthly housing costs and can significantly affect affordability.

How do interest rates affect home affordability?

Higher interest rates increase monthly payments and can reduce the home price you can comfortably afford.

What costs should I include besides mortgage payment?

Include taxes, insurance, HOA fees, mortgage insurance, maintenance, utilities and closing costs.

Which tool can estimate home affordability?

A Mortgage Calculator can estimate monthly payments using home price, down payment, loan term and interest rate.

About the author

The MuffinPost Editorial Team creates practical guides for online tools, calculators, finance basics, productivity and everyday digital workflows.