How Mortgage Interest Works

Learn how mortgage interest works, how lenders calculate it, what affects your rate and how to estimate your monthly payment with a free mortgage calculator.

Quick summary

Mortgage interest is the cost you pay to borrow money for a home. Your monthly payment usually includes both principal and interest. At the beginning of the loan, a larger part of each payment often goes toward interest. Over time, more of your payment goes toward paying down the loan balance.

Key takeaways

- Mortgage interest is based on your loan balance, interest rate and repayment term.

- Early mortgage payments usually include more interest and less principal.

- Your credit score, down payment, loan term and market rates can affect your interest rate.

- A mortgage calculator helps estimate monthly payments and total interest before borrowing.

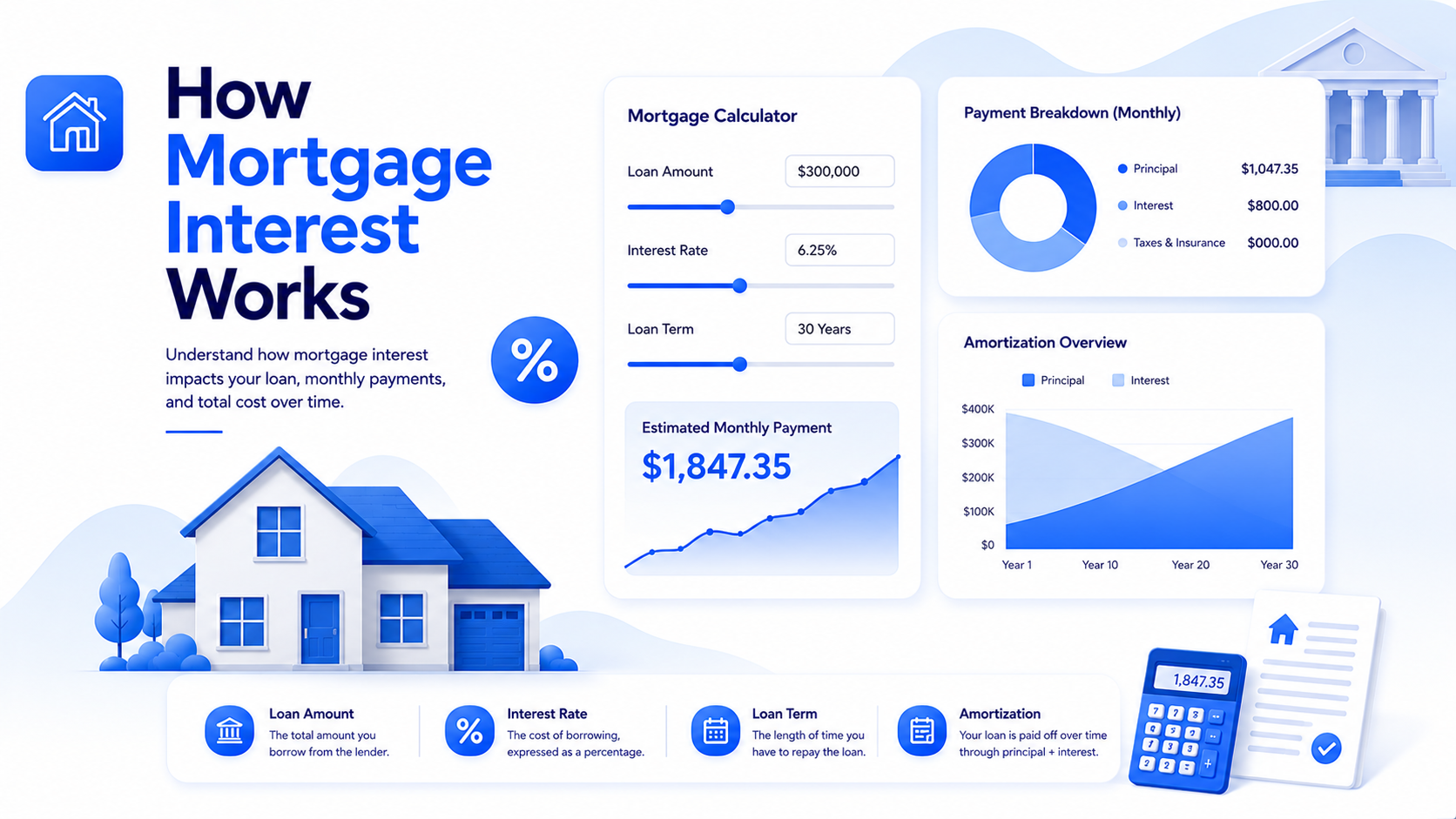

What is mortgage interest?

Mortgage interest is the amount a lender charges you for borrowing money to buy a home. When you take out a mortgage, you agree to repay the loan over time, usually with interest added to the original amount borrowed.

Your mortgage payment is commonly made up of principal and interest. The principal is the loan amount you still owe. The interest is the borrowing cost charged by the lender.

Principal vs interest

Principal reduces your loan balance. Interest does not reduce the balance; it is the lender’s charge for the loan. In many mortgage schedules, early payments are interest-heavy, while later payments pay down more principal.

How mortgage interest is calculated

Mortgage interest is usually calculated using your remaining loan balance, the interest rate and the payment schedule. Each month, interest is applied to the outstanding balance. As the balance decreases, the interest portion of future payments usually becomes smaller.

| Component | What it means | Why it matters |

|---|---|---|

| Loan amount | The total amount borrowed | Larger loans usually generate more total interest. |

| Interest rate | The percentage charged by the lender | Small rate changes can affect total cost significantly. |

| Loan term | How long you repay the loan | Longer terms lower payments but often increase total interest. |

| Payment schedule | How payments are applied over time | Amortization changes principal and interest portions each month. |

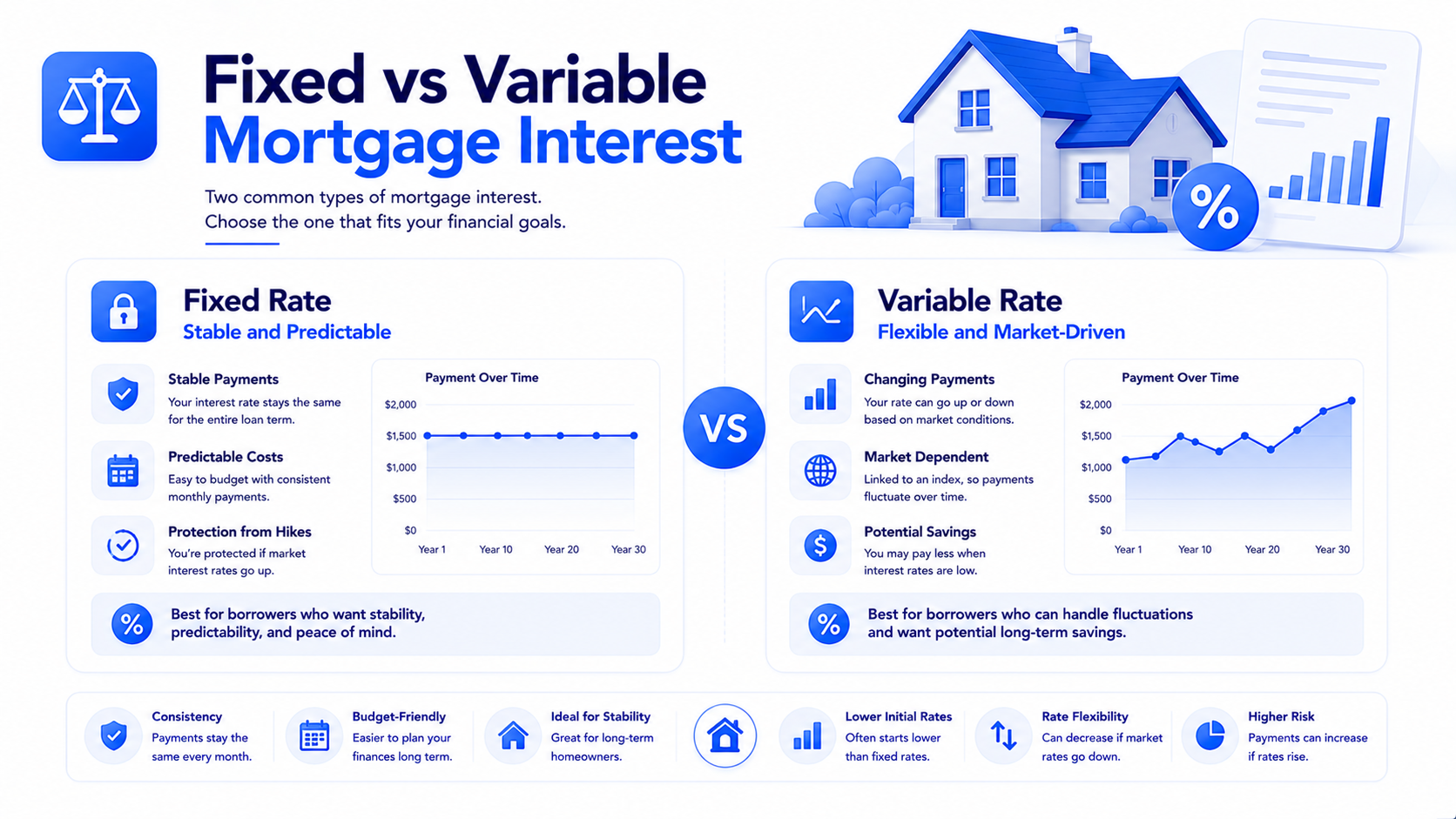

Fixed vs variable mortgage interest

Mortgage interest can be fixed or variable. A fixed-rate mortgage keeps the same interest rate for the loan period or selected fixed period. A variable or adjustable-rate mortgage can change based on market conditions and loan terms.

| Type | Main advantage | Main risk |

|---|---|---|

| Fixed-rate mortgage | Predictable payments | May start higher than some adjustable options. |

| Variable or adjustable rate | May begin with a lower rate | Payments may increase if rates rise. |

What affects your mortgage interest rate?

Your mortgage interest rate depends on several factors, including your financial profile, the loan structure and the broader market. Understanding these factors helps you compare offers more clearly.

Credit profile

A stronger credit profile may help you qualify for better interest rates.

Down payment

A larger down payment can reduce risk and may improve loan terms.

Loan term

Shorter terms often have higher monthly payments but lower total interest.

Common mortgage interest mistakes

Many borrowers focus only on the monthly payment and ignore the total interest cost. A payment may look affordable today but become expensive over the full life of the loan.

APR can include interest plus certain loan costs, making it useful for comparing mortgage offers.

Different lenders may offer different rates, fees and terms for similar borrowers.

A lower payment may come with a longer term and more total interest over time.

Mortgage interest best practices

The best way to understand mortgage interest is to compare scenarios before you borrow. Test different rates, loan terms and down payments to see how they affect monthly payment and total interest.

Compare multiple lenders

Small rate differences can change your total cost over many years.

Test loan terms

Compare 15-year, 20-year and 30-year scenarios to understand trade-offs.

Calculate total interest

Look beyond the first monthly payment and review the total borrowing cost.

Estimate your mortgage payment

Use The MuffinPost Mortgage Calculator Online Free to estimate monthly payments, compare loan terms and understand how interest affects your total mortgage cost.

Open Mortgage CalculatorBrowse CalculatorsFrequently asked questions

How does mortgage interest work?

Mortgage interest is the cost of borrowing money for a home. It is usually calculated based on the remaining loan balance, interest rate and repayment schedule.

Why do early mortgage payments have more interest?

Early payments are based on a larger outstanding balance, so more of each payment may go toward interest at the beginning of the loan.

What is the difference between principal and interest?

Principal reduces the loan balance. Interest is the lender’s cost for letting you borrow the money.

Is a fixed mortgage rate better?

A fixed rate offers predictable payments. Whether it is better depends on your goals, market conditions and how long you plan to keep the loan.

What affects mortgage interest rates?

Credit profile, down payment, loan term, loan type, lender policies and market conditions can all affect mortgage interest rates.

How can I reduce total mortgage interest?

You may reduce total interest by choosing a shorter loan term, improving credit, making a larger down payment or paying extra principal when allowed.

Should I compare APR or interest rate?

Both matter. The interest rate affects payment, while APR may include certain loan costs and can help compare offers.

Which tool can estimate mortgage interest?

A Mortgage Calculator can estimate monthly payments and total interest based on loan amount, rate and term.

About the author

The MuffinPost Editorial Team creates practical guides for online tools, calculators, finance basics, productivity and everyday digital workflows.